Blog

Content

Revenue up, margin down: how hotel owners can win back profit

The best competitive advantage is operational clarity: knowing where margins leak, which can be fixed without harming the experience, and which systems need to be redesigned.

Jurgen Schouten

Head of Sales

Hotel performance has often been viewed through the lens of a handful of commercial metrics such as occupancy, average daily rate (ADR), and revenue per available room (RevPAR). However, even when these numbers are strong, they don’t paint the complete picture.

Across many markets, hotel owners and operators are living a different reality. Revenues can look healthy, yet margins feel tighter. Cash feels harder to come by, renovations feel harder to finance, and every budget cycle starts with the same question: “Where’s the profit?”

A recent Skift feature clearly outlines this issue. The largest hotel brands have been highly profitable under asset-light models, while many owners, especially small and midscale operators, are being squeezed by rising operating costs, higher debt payments, and fee structures that pull from gross revenue even when profitability weakens.

This is not an anomaly; costs will continue to increase. It is a structural margin problem shaped by macroeconomic pressures and by the way modern hospitality economics distribute costs and risk among owners, operators, and brands.

Let’s have a practical look at why profits are being squeezed even when sometimes revenue is up, and where efficiency can be improved without taking anything away from the guest experience. Payments and distribution are a big part of that story, not because they are the only levers, but because they often hide a surprising amount of fees, friction, and manual work.

The margin squeeze

At the property level, hotel profitability is not simply revenue minus a few costs. It is a tight conversion problem: how much of each incremental dollar of revenue survives the “cost stack” to reach gross operating profit (GOP), net operating income (NOI), and ultimately distributable cash.

In the U.S., that conversion problem is being amplified by a refinancing squeeze. As of early 2026, AAHOA members have described a “$48 billion debt wall,” with many owners trying to refinance loans originally priced at 3%–4.5% that are now resetting above 6.5%, materially increasing carrying costs.

As a result, even modest changes in demand or expenses can hit distributable cash faster than operators expect.

When topline rises, but expenses rise faster, the conversion rate drops. CBRE’s analysis of a large sample of U.S. hotels highlights this pattern: in 2024, total hotel revenue rose, but operating expenses increased more quickly, and profit margins at both the GOP and EBITDA levels declined.

HVS makes a similar point, looking at budgets and priorities: as ADR growth flattens, revenue can no longer “absorb” cost increases as it sometimes did during the immediate post-pandemic rebound. The result is broad GOP compression driven by labor, insurance, utilities, and brand or operator-related expenses.

AHLA’s 2025 State of the Industry messaging also emphasizes that rising costs outpaced revenue growth in 2024, with several expense categories increasing nearly 5% year-over-year (YoY).

The exact mix varies by region and segment, but the pattern is consistent: the path from revenue to profit is narrowing.

When demand is down, the asymmetry gets worse. Owners feel the downside immediately: occupancy slips, labor stays expensive, debt service does not wait, and Property Improvement Plans (PIPs) still arrive on schedule.

But many of the biggest checks are calculated off gross revenue, not profit. So as margins compress, the tolls still get paid, and residual cashflow can collapse faster than the topline.

The macro and structural forces behind rising costs

Labor costs remain elevated, and efficiency gains are hard-won

Labor is often the most consequential line item in hotel operations and one of the most operationally complex. Even when teams improve productivity, wage pressure can still overwhelm those gains.

Recent labor data discussed on Hospitality Net, based on Hotel Data by Actabl, shows operators actively reducing hours per occupied room while wages rose, indicating a sustained effort to improve labor efficiency amid margin pressure.

The takeaway for both owners and brand executives is not simply “labor is expensive.” It is that labor flexibility is limited. Hotels are 24/7 businesses with service expectations that do not always scale down neatly when demand becomes more volatile.

Financing costs and debt service constrain options

Higher interest rates directly affect owners’ cashflow and investment decisions. When refinancing becomes costly, “good enough” cashflow can quickly turn into “not enough” cashflow.

The pressure is particularly acute where a large volume of loans are maturing at once (including CMBS exposure). With delinquencies rising and lenders less willing to extend credit, some owners are forced into expensive stopgaps, including very high-rate mezzanine debt, while still facing multi-million-dollar renovation mandates that absorb cash.

Skift’s reporting specifically cites higher debt payments, rising costs, and soft occupancy as factors pushing some owners toward delinquency or exit.

For finance leaders, this matters because margin compression is not just an operating statement issue. It quickly becomes a capital structure issue.

Fees and mandates tied to gross revenue can magnify pressure

A core tension in franchised and managed models is that many fees are calculated as a percentage of revenue rather than profit.

Skift highlights franchisee pressure from royalty fees based on gross revenue and renovation mandates, which can be difficult to absorb during periods of softer demand or rising operating costs.

This is not inherently “good” or “bad,” but it means that in a cost-inflation environment, owners can experience a compounding effect: revenue-linked fees rise with ADR, while many costs rise with inflation, and debt service remains stubbornly fixed.

Why “cut costs” is the right instinct, but the wrong framing

When leaders talk about cutting costs, there’s always a concern that service will suffer.

That’s not what the best operators do. They protect margin by building structural efficiency by removing friction that never improved the guest experience in the first place.

In practice, that looks like:

Cutting avoidable admin work

Reducing errors and exception handling

Automating workflows that shouldn’t require humans

Making cashflow and reconciliation more predictable

Lowering “taxes on revenue,” like unnecessary fees and leakage

The goal is to do less manual work, make fewer mistakes, and keep more of every dollar you earn.

Payments: the lever that touches owners, brands, and finance teams

In many hotel P&Ls, payment-related costs are spread across categories, which makes them easier to ignore. But payments are often a compound cost that includes:

Processing fees

Chargebacks and fraud losses

Payment failures and rework

Manual reconciliation and investigation

Time spent chasing missing remittance data

Cross-border and foreign exchange (FX) complexity (in many business-to-business (B2B) flows)

Doug Rice put it bluntly in a Hospitality Upgrade column: hotel payments are unusually complex and, compared to other industries, have lagged modern best practices, leaving meaningful money on the table.

This matters because payment friction behaves like a margin leak. It quietly reduces profit in small increments and consumes staff time. In a world where labor is already expensive, “time spent fixing payments” is not just a nuisance. It is a cost.

Distribution: the other “tax on revenue”

Payments are not the only area where margin quietly leaks. Distribution is another structural source of leakage because many distribution costs scale directly with revenue.

Distribution is not just “OTAs are expensive.” It is a broader set of cost and workload drivers that includes:

OTA commissions and merchant margin (which often show up as a direct haircut to room revenue)

Meta search and digital marketing costs needed to win demand (which can rise as competition increases)

GDS fees and agency commissions in corporate segments

Channel management and connectivity fees, plus the operational burden of maintaining multiple integrations

Rate parity, content, and mapping issues that create exceptions, disputes, and lost conversions

Manual reconciliation of bookings, invoices, and remittance data across multiple intermediaries

Like payment friction, distribution friction creates a double hit:

Hard costs: commissions, fees, and margin that never reach the property.

Soft costs: time spent managing exceptions, disputes, mapping problems, and settlement questions.

This matters because when ADR rises, the “take rate” can increase as well. And when demand softens, the mix can shift toward higher-cost channels, increasing distribution drag precisely when hotels need conversion the most.

In down cycles, that asymmetry shows up fast: the take rate can rise while cashflow falls.

What efficient payments look like

Efficient payments are not about forcing one payment method everywhere or optimizing fees at the expense of control and trust. They are about designing payment, settlement, and reconciliation flows (across both guest and intermediary contexts) that are:

Lower-cost by default

More automated end-to-end

Easier to reconcile

Removes payment from the front desk, reducing payment friction.

Better aligned with how hotels actually operate

Any process that routinely creates exceptions must be redesigned. And payments are among the most error-prone processes in hospitality.

What efficient distribution looks like

Efficient distribution is not about eliminating intermediaries overnight or forcing every booking into one channel. An effective distribution strategy will:

Lower leakage by default (fewer unnecessary layers and fees)

Increase direct channels, which grow brand value and improve the guest experience

Create more transparency (clear economics by channel and partner)

Make it easier to reconcile end-to-end (consistent identifiers and settlement data)

Be less exception-prone (fewer mapping and parity issues)

Be more aligned with how hotels actually operate

Any channel or partner flow that repeatedly causes disputes, mapping errors, or reconciliation issues needs to be changed or reconsidered.

Change must occur on the foundational level

Infrastructure matters here because payments and distribution are not two separate problems. They are two parts of the same commercial flow.

A booking does not stop being “distribution” when it is confirmed, nor does it become “payments” only at check-in. The same transaction moves through pricing, channel partner economics, confirmation, settlement, and reconciliation. When distribution and payments run on different rails, hotels get stuck with:

Duplicated integrations and intermediaries

Inconsistent identifiers between booking, invoice, and settlement

Missing or delayed remittance data

More disputes and exception handling

A larger gap between what was sold and what gets reconciled in the books

That is why meaningful change requires a single, end-to-end platform layer in which distribution and payments run on the same infrastructure and data model.

When distribution and payments are designed as one flow, the industry can:

Create the conditions to reduce fee stacking across intermediaries by making channel economics and payment costs visible and optimizable together.

Tighten the data chain so booking, remittance, and settlement share consistent identifiers from start to finish.

Automate reconciliation (and speed up close) by ensuring the data finance teams need is generated as part of the transaction, not reconstructed after the fact.

Shrink the exception surface area by preventing the most common mismatch points: mapping issues, parity disputes, missing references, and failed or delayed settlement.

For owners and asset managers, the outcome is improved profit conversion.

For brand and operator executives, it is smoother operations without service degradation.

For finance leaders, it means fewer unreconciled items, clearer visibility, and less time spent resolving exceptions.

It is not the only lever in the toolbox. But it is one that can reduce both “hard costs” (fees) and “soft costs” (time) in the same motion.

A playbook for increasing margin

If revenue growth is slowing while costs remain persistent, the strategic response is to focus less on topline ambition and more on conversion discipline: converting revenue into profit, profit into cash, and cash into optionality.

Based on the pressures seen across recent industry reporting and analysis, a few themes consistently show up in resilient operators’ playbooks:

Benchmark cost categories and track them in the same way as revenue key performance indicators (KPIs).

If expenses above and below GOP are rising faster than revenue, leaders need visibility early, not at month-end.

Build a simple “conversion dashboard” that ties RevPAR growth, gross margin, GOP margin, and NOI together, so leaders can see where the drop-off occurs.

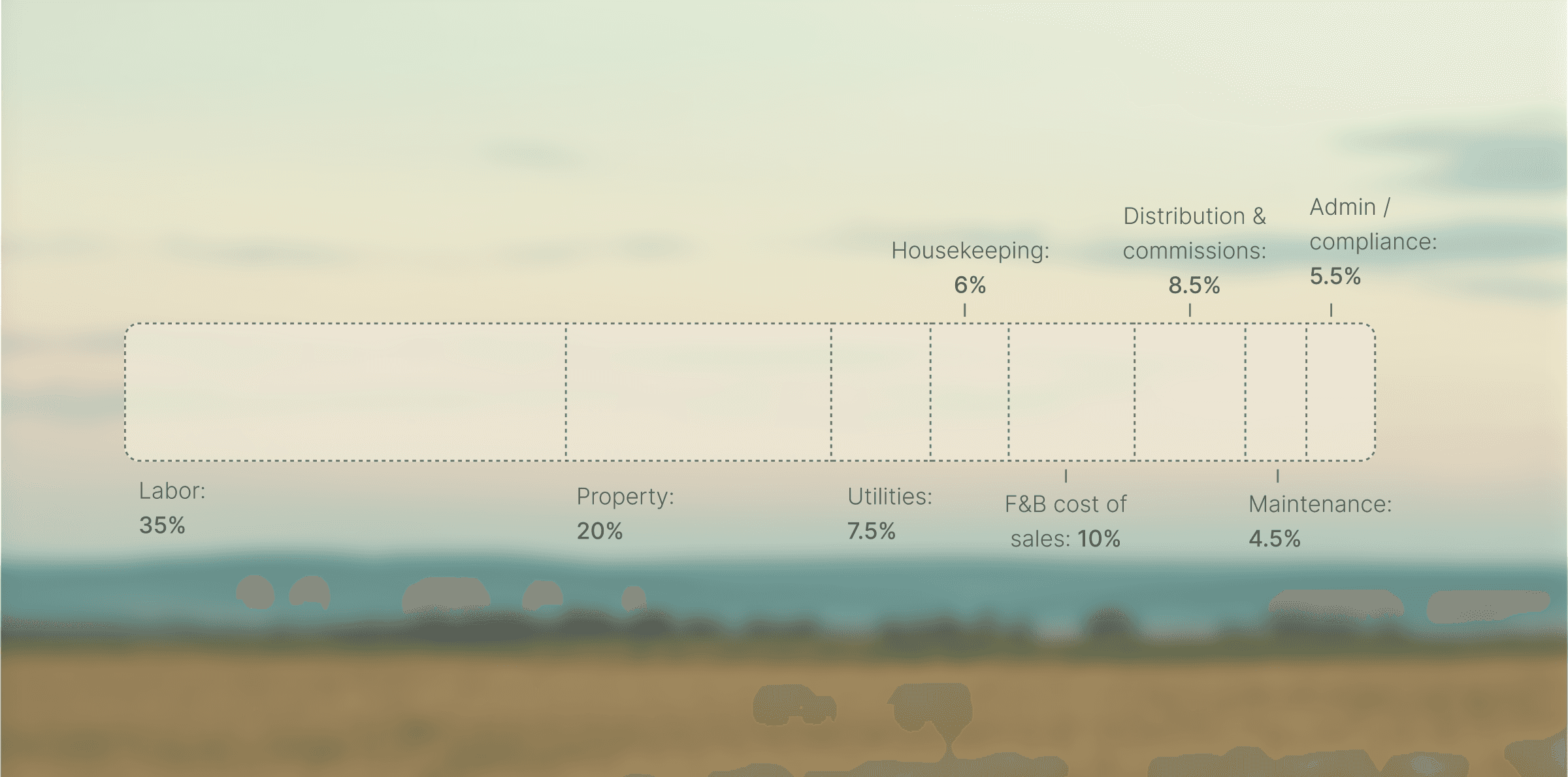

Break the cost stack into a small number of buckets that map to operational levers: labor, utilities, insurance, online travel agency (OTA) and distribution, brand and management fees, and maintenance.

Track rates of change, not just absolute spend. If insurance is up 12% YoY while revenue is up 4%, the problem is visible early.

Treat cost variance analysis like pickup reporting: weekly reads on the biggest swing categories, with owners and operators aligned on action thresholds.

Make labor efficiency a continuous operating discipline.

Even small changes in hours per occupied room can matter as wages rise.

Manage productivity metrics that link staffing to demand patterns, including hours per occupied room, rooms cleaned per attendant-hour, and check-in volume per front-desk hour.

Standardize “flex” playbooks by day of week and occupancy bands so managers do not reinvent schedules each week.

Reduce the work, not the service: remove low-value tasks, simplify standard operating procedures (SOPs), and automate where it prevents rework (e.g., payment exception routing, remittance matching, invoice-to-booking reconciliation, chargeback handling, and channel exception resolution).

Identify the labor that is actually caused by exceptions, such as payment failures, disputes, distribution mapping and parity issues, and reconciliation gaps, then eliminate the root causes so the hours disappear sustainably.

Treat fees on gross revenue as a strategic constraint.

If fees and mandates scale with revenue, the organization needs to offset this elsewhere to keep profit conversion stable.

Make fee drag visible by translating every major fee category into basis points of revenue and percent of GOP, then track the trend as ADR changes.

Model scenarios in which ADR rises while occupancy softens. In those cases, revenue-linked fees may hold steady or rise while variable costs do not fall as much as expected.

Treat mandated capex and brand standards as part of cash planning, not just a compliance checklist. The key question is whether the property can self-fund without starving the business.

Where contracts allow, renegotiate service levels, timing of mandates, or fee structures that are misaligned with market reality. Where they do not, they plan to compensate elsewhere.

Fix payments and distribution as levers for structural efficiency.

Payments and distribution both touch cost, risk, and labor. Legacy approaches create leakage and work. Modernizing payments can reduce both, and improving distribution economics and data flow can do the same.

Quantify the full payment cost, not just processing rates: include dispute handling, failed transactions, manual matching, missing remittance data, and write-offs.

Quantify distribution cost as a “tax on revenue” by channel: commissions, connectivity fees, marketing spend required to win demand, and the cost of exceptions.

Reduce exceptions by design. Any flow that frequently causes mismatches among booking, remittance, and settlement data (or creates mapping and parity disputes) should be rebuilt to use consistent identifiers and automation.

Improve cash predictability by tightening settlement timing and reconciliation, so finance teams spend less time in investigation mode and more time on forecasting.

Prioritize the highest-friction B2B and intermediary-heavy flows first, where fee stacking, cross-border complexity, and manual reconciliation are most painful, and where operational fixes can quickly show up in GOP and working capital.

Operational efficiency is vital to success

Hospitality has always been a demanding business, and now, the margin for error is smaller than ever. When costs rise and growth flattens, the winners are not simply those who drive the most demand. They have the most disciplined conversion story.

Revenue will always matter. But in the next phase of hospitality, the most durable competitive advantage may be operational clarity: knowing where margins leak, which can be fixed without harming the guest experience, and which systems need to be redesigned rather than patched.

That is the lens that owners, brand executives, and finance leaders can align around, even when their incentives differ. In a world of persistent cost pressure, hotels that operate efficiently will be the ones that stay healthy.

Jurgen Schouten

Head of Sales

Share